Key Takeaways

- No universal model: The right choice between a points program, cashback, and a status model depends on the retailer's purchase frequency, gross margin, and target group structure.

- Consider hidden costs: Breakage effects with points, margin pressure with cashback, and churn risks with status models significantly impact real profitability.

- High market penetration: According to a GfK study commissioned by Mastercard , up to 90% of Germans use bonus programs at least occasionally. The question is not whether, but which concept delivers the highest ROI.

- Flexible Implementation with Convercus: As a modular loyalty platform , Convercus enables the native implementation of all three models within a single omnichannel infrastructure, including hybrid models.

Collecting points, cashback, or exclusive tier benefits: Anyone responsible for loyalty in retail facing this decision knows it's about more than just mechanics. A wrong decision ties up budget, IT resources, and team capacities for years. Convercus, as a loyalty software provider, has natively implemented all three models and integrated over 6 million customers for a single brand in a very short time. In this guide, we categorize these concepts from an operator's perspective: how they work, their actual cost structure, decision-making aids for each retailer profile, as well as tax and data protection legal frameworks. This will help you identify the right loyalty concept for your business model – with concrete cost and ROI estimates from an operator's perspective.

Points Program vs. Cashback vs. Tier Model: Mechanics, Costs, and Customer Impact

Three core concepts dominate the loyalty landscape, each following its own logic:

- Points programs rely on deferred rewards: customers collect points and later redeem them for rewards or rebates. Points programs retain customers through deferred rewards, and typical redemption rates range from about 20% to 60% depending on the program, but can be higher in optimized cases.

- Cashback models provide immediate euro rebates, directly after purchase, typically 0.5–2% of sales.

- Tier models differentiate customers through tiered systems with exclusive benefits.

From an operator's perspective, companies strategically manage cost structures and customer behavior through point values, expiration dates, and tier thresholds.

What Does a Points Program Really Cost? Breakage Effects and Balance Sheet Provisions at a Glance

The so-called breakage effect describes the proportion of collected points that are never redeemed.While this might sound like pure profit, it isn't. As long as points are valid, companies must account for them as a liability on their balance sheet. . For example, with Payback, points expire after 36 months,which leads to the dissolution of balance sheet provisions. Breakage rates typically range from about 10% to 40%, depending on design and user activity. The expiration period is therefore not a minor detail, but a central control element for costs and the balance sheet.

Points programs are most effective for retailers with high purchase frequency: Groceries,, Drugstores, and Fashion are classic application areas. A wide product range creates diverse redemption opportunities and increases perceived attractiveness. The psychological driver behind this is the urge to collect,reinforced by gamification elementsthat regularly motivate customers to make repeat purchases.

When is Cashback Worthwhile for Retailers – and When Does It Eat Into Margins?

Cashback directly and immediately impacts margins. With typical cashback rates of about 0.5–2% in card-based environments, this quickly becomes critical for low-margin assortments. In e-commerce or affiliate models, however, rebates can be significantly higher.

A concrete example: If a grocery retailer offers 1% cashback with a gross margin of only 3%, only 2% remains. With rising operating costs, this difference can jeopardize the contribution margin. The direct margin impact therefore makes cashback a risk factor in the grocery retail sector..

Advantages and Disadvantages of Cashback for Retailers at a Glance:

How Do Tier Models Reduce Churn? Churn Prevention Through Exclusivity

Tier models leverage one of the strongest psychological levers: loss aversion.Once someone has achieved Gold or Platinum status, they don't want to lose it. Tiered systems like Silver, Gold, and Platinum create a dual incentive:to reach the next status or defend the current one. This is coupled with a feeling of exclusivity. These mechanisms can increase customer loyalty and reduce churn, especially in industries with high emotional attachment, as switching to a competitor is perceived as a loss.

Tier models are particularly effective with low purchase frequency but high basket value. Typical application areas include:

- Premium Retail

- Hospitality

- Travel

- Automotive

In these sectors, simply collecting points would be too slow to be motivating. Miles & More and BahnBonus demonstrate how status-driven customer loyalty works over years, permanently tying customers to a brand.

.png)

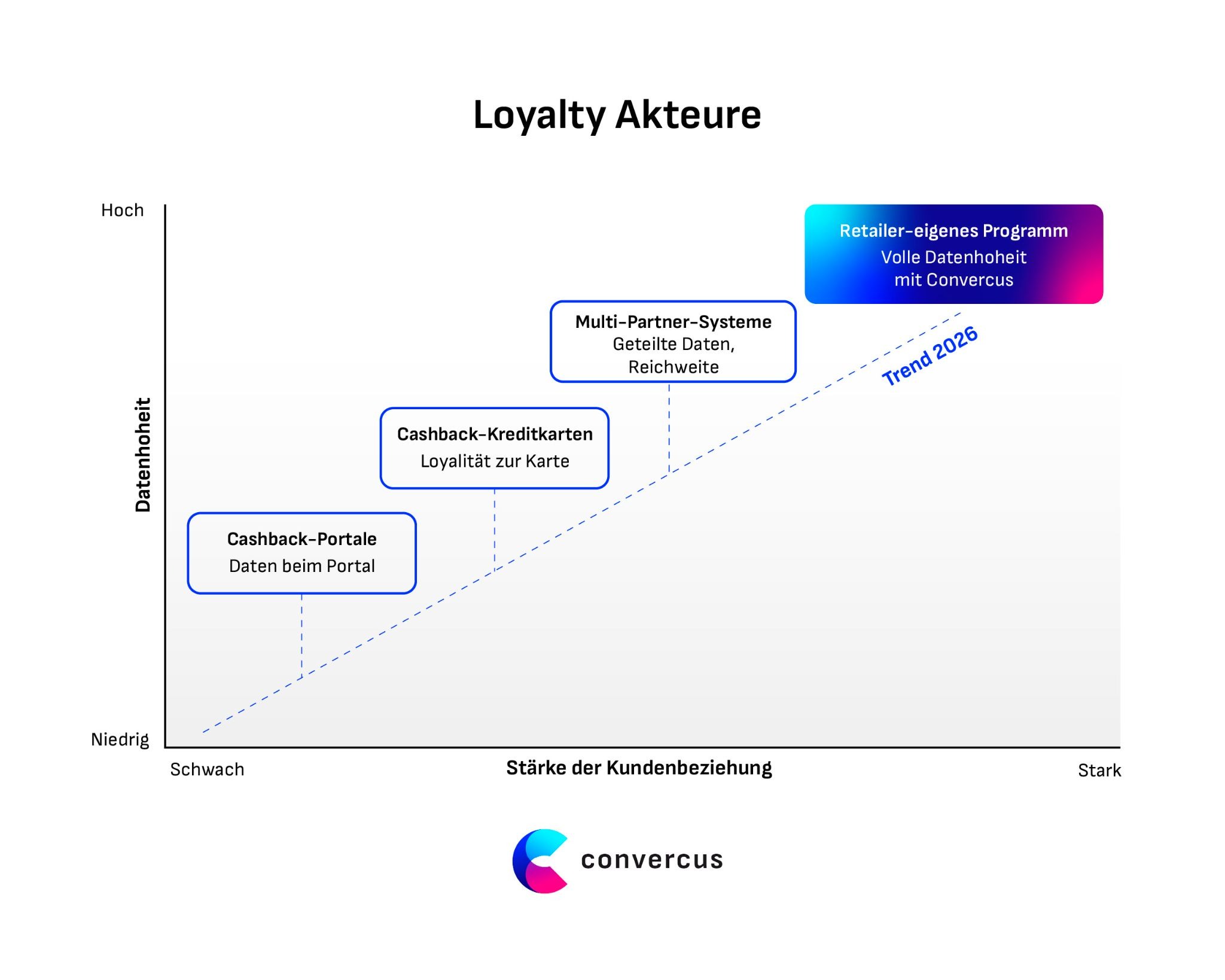

Own Program or Multi-Partner: How is the German Loyalty Landscape Evolving in 2026?

The German loyalty landscape is undergoing a paradigm shift. For years, reach was the most important argument for multi-partner systems like Payback. Now, another factor is coming to the forefront: data sovereignty.REWE and Penny have deliberately separated from Payback and established REWE Bonus, their own bonus program. The signal is clear: large retailers want to regain control over customer data and customer engagement.

At the same time, Edeka is taking the opposite approach and switching to Payback.This is a classic make-or-buy decision in favor of reach and immediate market penetration. Both strategies are valid. However, the implications for data sovereignty, CRM control, and long-term enterprise value are fundamentally different. It's no longer just about collecting points vs. cashback. The central question is: Who owns the customer relationship?

Cashback Credit Cards: Competition for Your Own Customer Relationship?

Providers like American Express, Revolut, or co-branded credit cards are increasingly inserting themselves as an additional layer between retailers and customers. Credit cards with cashback or bonus points complement customer loyalty – but can also overshadow the direct relationship with the store if loyalty is primarily tied to the card.

Cashback Providers: Affiliate Platforms as a Marketing Channel or Margin Eaters?

Cashback providers like Shoop, TopCashback, or iGraal operate on a simple principle: the retailer pays an affiliate commission, and the portal passes on a portion as a rebate to the customer. This can be effective for new customer traffic in online retail in the short term. In the long term, however, such cashback providers result in permanent commission payments with every purchase, and data sovereignty over customer behavior remains with the portal..

The Strategic Check for Retailers: At what customer volume does an in-house loyalty system become more cost-effective than continuously sharing commissions with cashback platforms? With a usage- and success-based pricing model, such as that offered by Convercus, an in-house program becomes more economical than ongoing affiliate costs beyond a certain size. Simultaneously, the retailer regains full control over customer data and customer engagement.

Decision Aid: Which Loyalty Concept Suits Which Retailer Profile?

Choosing the right model is not a matter of taste, but a business decision. It depends on three key variables: purchase frequency, gross margin, and target group structure.The following decision matrix assigns the appropriate loyalty concept to six typical retailer profiles and provides the business rationale.

Two crucial framework conditions for decision-making are often overlooked when choosing a model:

Firstly, the tax exemption limit: Cashback is generally treated as a discount for tax purposes and is therefore not subject to income tax. Tax liability may arise if payments are not directly related to a purchase (e.g., referral bonuses according to § 22 No. 3 of the German Income Tax Act). Retailers must ensure that their reward distribution meets compliance requirements.

Secondly, the GDPR requirements: Points programs require extensive data processing. Legal bases, rights of access under Art. 15 GDPR, and data minimization must be ensured from the outset. Both aspects directly influence the choice of model.

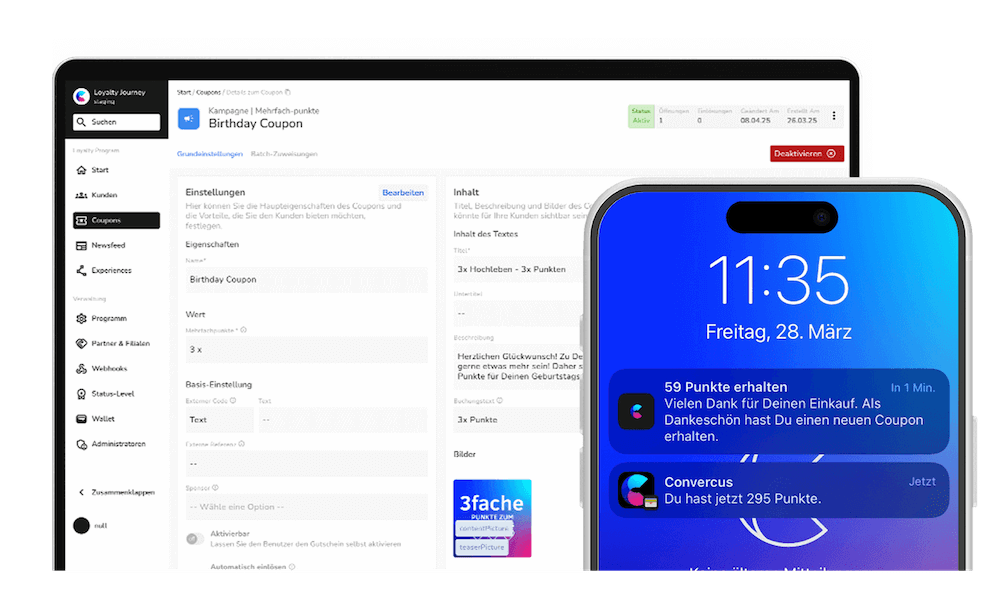

This is precisely where the advantage of a modular customer loyalty software like Convercusbecomes apparent: All three concepts (points, cashback, and status model) can be natively mapped in one system. Retailers do not have to commit to a single model in advance. Hybrid models, such as points combined with status or couponing can be flexibly built and adapted without having to switch platforms. The usage-based pricing model also allows for a gradual entry: start small, scale when the results are right.

From Concept to Implementation: How Convercus Unites Points, Cashback, and Status in One System

The strategic analysis is complete, the decision matrix shows which model suits which retailer profile. The crucial question remains: Who implements all of this technically and strategically? As a modular loyalty platform, Convercus combines points programs, cashback, and status models in a single omnichannel infrastructure. The Loyalty Engine natively maps points, status, and rewards. It is complemented by powerful couponing and seamless integration via POS, online shop , and whitelabel app. This creates a consistent system that connects all channelsinstead of creating isolated silo solutions.

All Convercus features at a glance:

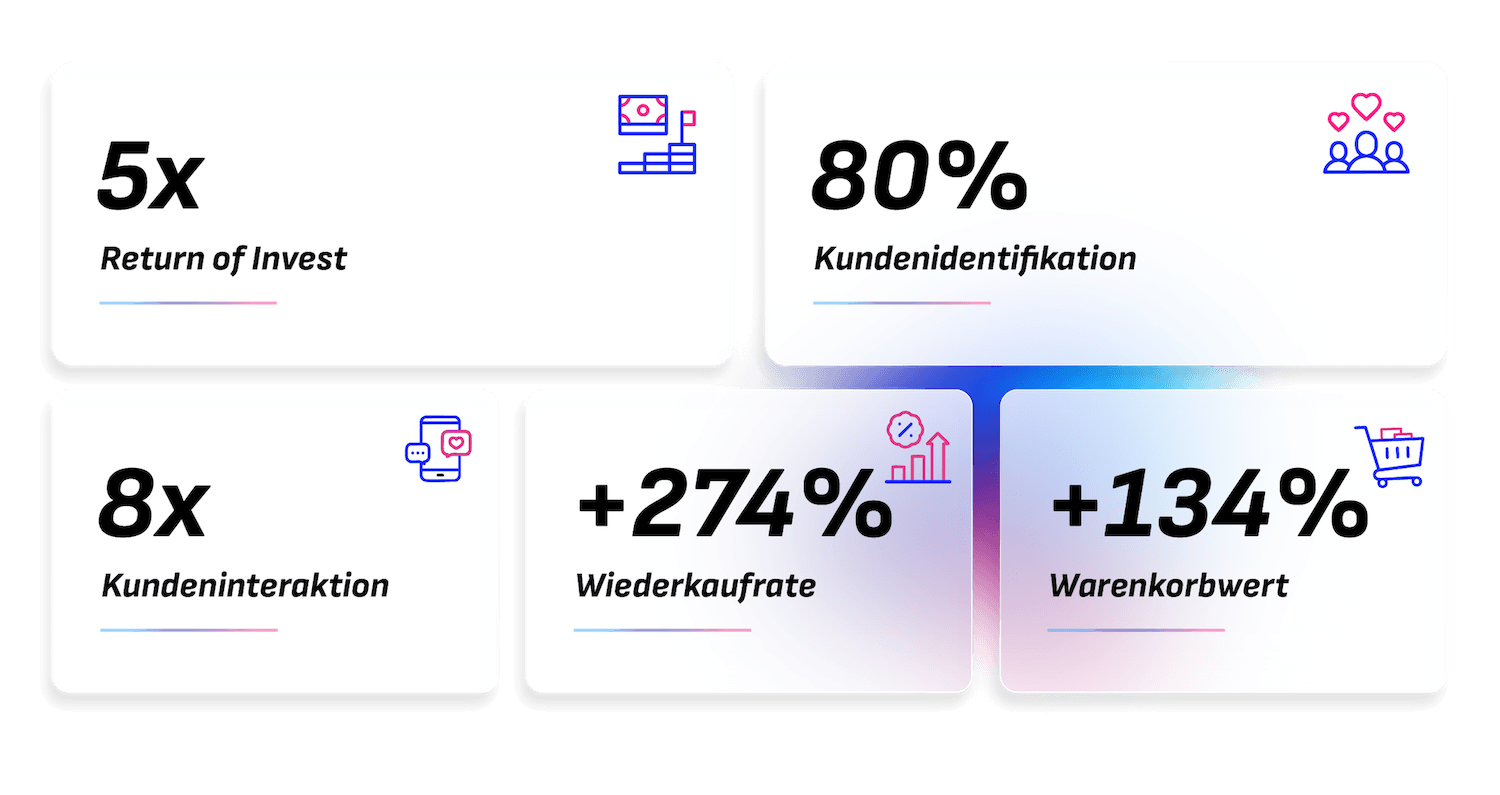

- Over 6 million customers integrated into one program for a single brand

- Up to 80% redemption rate for collected points

- 8 times higher customer interaction with a whitelabel app

- API-first approach with minimal IT resources

- Usage-based pricing model with low implementation costs

- 100% GDPR compliant with full data sovereignty for the retailer

Convercus not only provides the technical platform. Through proven success management, the team also supports strategic program design: from conception and rollout to ongoing optimization. This transforms a software implementation into a true partnership that delivers measurable results. Launching a loyalty program becomes effortlessly easy.

FAQ

What tax exemption limits apply to loyalty rewards in B2C retail?

Cashback is generally considered a discount and is therefore not subject to income tax, provided it is directly related to a purchase. Referral bonuses or rewards without a direct purchase connection, however, are classified as other income under § 22 No. 3 of the German Income Tax Act. These remain tax-free up to €256 per calendar year.

How do expiration dates affect the accounting of points?

Unredeemed points must be accounted for as a liability. Typical expiration periods are 24–36 months. This so-called breakage is a strategic control element: it limits provisions on the balance sheet while simultaneously creating opportunities for customer re-engagement through targeted "points expiring soon" communications.

What are the risks of "coupon stacking" from an operator's perspective?

When customers combine points programs, cashback credit cards, and portals, the effective discount can exceed 7%. This uncontrolled accumulation significantly jeopardizes the gross margin. A dedicated loyalty platform like Convercus enables flexible rule sets that specifically manage stacking.

GDPR in Loyalty Programs: What Data Sovereignty Do Retailers Need?

Loyalty programs process personal data such as purchase history, preferences, and contact details. Retailers need a clear legal basis, must ensure rights of access under Art. 15 GDPR, and data minimization must be ensured. A first-party data strategy with its own system increases long-term business value compared to shared data in multi-partner systems.

Why relinquish margins and data to third-party platforms? With Convercus, you build your own highly profitable loyalty infrastructure – tailored to your goals and without unnecessary fees.

For retailers, a pragmatic look at the overall structure is worthwhile: card payments incur fees and generally don't provide direct access to customer data. While external bonus cards or multi-partner programs like Payback can increase reach and customer acquisition, their use requires a clear strategy regarding which data and customer relationships remain with the retailer. An in-house program specifically directs budget towards direct customer relationships and strengthens the first-party data foundation. These two approaches are not mutually exclusive: many retailers combine their own loyalty system with the reach of external platforms.

- Protect margins: Smart control instead of blanket discounts.

- Secure data sovereignty: Manage customer relationships without third-party platforms.

- Maximize ROI: Find the optimal model for your industry.